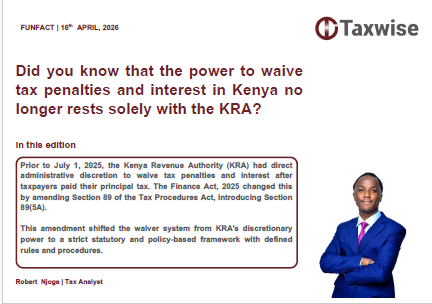

Before the amendment

of Section 89 of the Tax Procedures Act introduced by the Finance Act, 2025

which took effect on 1st July 2025, the Kenya Revenue Authority

(KRA), through the Commissioner of Domestic Taxes, exercised direct administrative

discretion to waive penalties and interest once a taxpayer had settled the

principal tax. However, the enactment of Section 89(5A) of the Tax Procedures

Act by the Finance Act, 2025 fundamentally altered this position by shifting

the waiver regime from administrative discretion to a tightly defined statutory

and policy‑driven framework.

16th Dec 2025

24th Nov 2025